Gold is highly-prized as a store of value. However,there are factors that leads to a drop or spike in its price. Let’s look at these closely.

Gold is used all

over the world as a store of value. Gold price is oft referenced because it is

continually traded, and this has been so for thousands of years. The spot price

might fluctuate with market conditions, but it is judged as highly valuable

Here, we are going to analyze the nine factors that affect the price of gold for for investors who might be interested in gold trading.

Global Crisis

Global economic

and political factors affect the price of gold because it is considered the

source of geopolitical and economic turmoil. When people lose confidence in

their governments or market, the price of gold tends to rise, and the reassurance

with their situation softens the market price.

Inflation

The prices of

gold may fluctuate but what you can buy with it remains stable for a long time.

Hence, holding gold is used as a hedge against currency devaluation and

inflation. Investors buy gold for holding when they can project that the value

of their paper money is going to decline.

Value of the U.S. Dollar

The U.S. dollar,

one of the main currencies for international trade, has an inverse relation

with the price of gold. When the gold is strong dollar is weak and vice versa.

Central Bank Instability

When the central

banks and other dominant banks go through a deficit problem, the paper currency

tends to lose its value. Therefore some investors see holding gold as a way to

protect their wealth ,which invariably boosts the demand and price of gold.

Interest Rates

When the

interest rates increase, people trade their gold to get funds for other

investment opportunities. When the interest rates decrease, the gold price goes

up again because of low opportunity cost in gold holding compared to other options.

Government Reserves

Central banks

hold gold as a reserve currency along with their paper money. When they buy

more gold than they are selling, this takes the prices of gold higher.

Jewelry and Industry

Not just a

valuable investment but half of the demand for gold is for jewelry from around

the world. India and China have huge gold reserves. About twelve percent of

gold demand comes from its industrial application.

Gold Production

Annual gold

production is about 2,500 metric tons while annual gold supply to the world is

estimated to be 165,000 metric tons. The cost of production can influence the

price of gold. When the production cost rises, miners sells out their gold to

get the benefit.

Supply vs. Demand

By simple

economic rule, when the demand for gold in the market increases the prices also

rise high. However, unlike other currencies, the price of gold remains fairly

stable for a long time and the fluctuations might be due to currency fluctuations

or some uncertainties.

Conclusion

Gold will endure

in the realm of men for a long time. With its value and occurrence remaining highly

-prized, you can sure its worth will continue to soar.

IRAs are important as they undergird the future for the working class. What if your IRA company goes bankrupt? What will you do? Read on to find out more.

My Gold IRA company went bankrupt. What now?

It’s a nightmare scenario for

most people, particularly those close to retirement: They’ve made investments

all of their lives to secure a future, but suddenly the company keeping them

says they have no money.

What happens now? Is everything

going to be fine, or have you lost all your savings and have to start over

again?

We’ll start with the good news:

In most cases, your savings will be covered by government-mandated insurance.

Note how we say most.

How insurance works on IRAs

The US government mandates that all IRA accounts need to be covered for at least $250,000. This cover is expected to be used in cases of funds going missing, as could happened during massive disasters.

If your company closes and for some reason your investments aren’t there (but they’re in the books) you should be covered. You should also be covered if your company falls victim to a robbery that funnels its funds, including the retirement funds and investments of its clients.

The $250,000 number is also a baseline – many IRA companies have insurance for two, three, or even ten times that much. Even if it’s a gold IRA, that should cover your IRA savings. Plus, we have a small detail with gold bars: They’re physical, bullion bars that should still be there anyway.

How gold bars make it simple

Any decent IRA provider will also refuse to be the sole custodian. Instead, most gold bars are kept in secure locations under tight government regulation, such as the Delaware Depository.

As long as your gold IRA puts your bars there, you should still have your investment even if the company disappears. Gold, after all, isn’t liquid and can’t be spent by accident, nor would it be at all easy to funnel gold bars from the facilities where they’re stored.

In most cases, what would happen

is that the government would contact you to arrange a transfer of funds towards

different management. Another company would take over, and you would barely

feel the change. Great, isn’t it?

Well, that’s only if the bankruptcy

is due to lack of funds. Things can get much more complicated if there’s fraud

involved.

What about IRA fraud?

Most people investing in their

IRA never get to see their shares, valuables, or even savings in physical form.

They just see numbers on a screen or paper representing them, and assume the

company is keeping them safe.

In most cases, companies do keep those things safe and transparently. However, it’s not unheard of for the management of a company like these to get a little bit happy about how funds are managed and on occasion tap onto them. Sometimes, tapping onto them often enough to make the company go broke.

If that’s the case things get a

bit more complicated, depending on your actual standing.

Is your IRA company legal?

This is the question that will drive what happens then. If your IRA company was legally registered with the IRS and followed with its regulations – that is, if the company was legal to the government’s eyes, – you’re in luck.

You should be able to retrieve your investments without more than a headache or two. If you’re a victim to IRA fraud in a company the government considered legal, government-backed insurance will kick in.

It’s more complicated if you put

your money on an unregistered IRA.

Unregistered IRAs are by

definition illegal, and therefore you won’t be covered by any laws that protect

IRA customers in these cases. If you put your money on an unregistered IRA you

have been the victim of fraud, as the money is gone and there’s no insurance to

back it up – nor will there be trustable books to confirm what you had.

In this case, a very long

investigation will likely take place, where the IRS will try to ascertain how

much each of the victims had stolen from them and in what form. If you’re

lucky, they’ll be able to salvage enough from the criminal’s assets to pay you

back.

You’re not likely to get lucky.

In most cases, the criminal will

have either already spent the money or funneled offshore into banks and

investments that can’t be tracked or confiscated. In this case, it’s more

likely than not that you will, in fact, have lost everything.

The takeaway: Avoid IRA fraud at all costs

One of the most important

decisions you’ll make about your finances will be your IRA manager and

custodian, precisely because of this. Your IRA money is only safe if your

company is legal. As such, you must do your homework before signing up with

anyone. Get references. Ask around. Investigate. Even calling the IRS to make

sure the company is in the clear might be necessary.

Do all that, simply because that

will give you peace of mind. Having a properly registered IRA manager will

protect you against anything that could happen with that money. Don’t take

risks with your future, and only put your investments in the hands of people

who have the legal clearance to manage it.

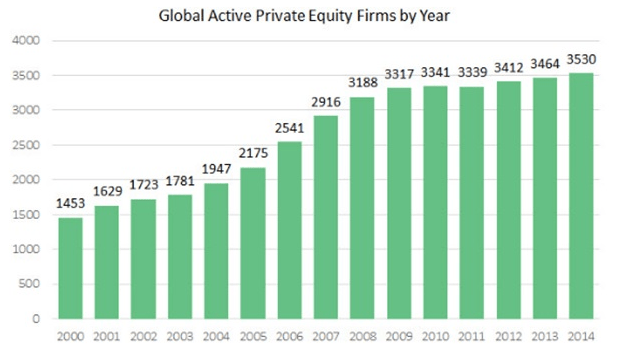

Private equity firms are growing by the numbers in today’s world. What do they do? How can they make a difference? Read on..

Private Equity Firms: What are

they?

The investment market isn’t immune to trends. While most trends come in the form of specific stocks, values, or markets to invest in (for example, cryptocurrencies,) there are always outlier trends, trends that aren’t so much expectations about the market but tricks and methods to optimize investment.

Sometimes, these trends are sold as ways to make people rich quickly with a minimal amount of work.

Private equity firms are one of the trends we see currently. The concept itself has been in the news often, usually blaming them for people getting laid off or praising them for creating new jobs, with most people unable to understand just what equity firms do.

How do these firms work?

A private equity

firm is, to put it simply, a conglomerate of investors who get together to

purchase companies or businesses in a private manner – that is, outside the

stock markets. The earnings these businesses receive (i.e., the equity) is then

divided among those investors who chipped in to take over the company.

Although simplistic, that’s basically how it works: A bunch of people with money get together, pool their money into a private equity firm, and share both the risks and the proceeds of such venture.

Usually, this is done through already existing private equity firms, although it’s not uncommon for individuals to start their own.

Are they good or bad?

As with

everything in business, this will depend on who you ask – and the specific

private equity firm you look into. In theory, a private equity firm taking over

shouldn’t be any different than having a new board of investors for publicly

traded companies. After all, that’s literally what such takeovers mean.

However, the experience many workers have had with these firms is quite different. While it’s no secret that public investors often try to get the most money they can out of businesses, there are two sides to the stock market that keep these attitudes relatively in check.

First, who owns

how much of each company is known. And second, the most valuable companies in

the stock market (say, Amazon or Apple) are mainstays and it’s in the

investors’ best interests to sacrifice short-term gain for long-term stability.

This is not necessarily true of private equity firms. The relative anonymity these firms give allows certain savagely capitalistic players to act in ways that, were they to be made public, would likely damage their images – and those of their companies.

Private equity firms effectively lessen this, because it’s often impossible to know who is behind the company.

There’s a second

issue, although closely related. Private equity firms are known for often

acting in extreme ways once they take over, sacrificing long-term stability for

short-term earnings, often forcing companies to cannibalize themselves and

their own market.

This leads these companies that have been

taken over to end up bankrupt, its employees laid off, all to fill the pockets

of people who already had much more money than the company’s workers.

Is there an upside?

One might argue that the operating strategy that these firms use could lead to better economic development, as many of the pressures of public trading, such as stock price variations, don’t exist.

And that is true. A properly managed private equity firm can indeed help a company, or a whole industry, flourish under the guidance of leading experts.

However, this doesn’t always happen – partly because some of the biggest actors in the market are only in it for the money, with little interest in making things better.

Conclusion

The fact that some firms are there to drive companies to the ground doesn’t mean they all will. Some private equity firms will indeed act in ways that will better the market, and we can hope with time the good companies will outweigh the bad.

IRAs are gaining attention around the globe. How best can you optimize them? That is the subject of this guide.

Best Hacks On Self-Directed IRAs

In order to understand the basic

misconceptions about the IRA, we first need to have a full grasp of what an IRA

is, and what is the major difference between traditional and self-directed IRA.

An IRA or Individual Retirement

Account is a way to save money for post-retirement with tax-free benefits. It

is an investment option designed for building saving funds for the time of your

retirement.

The concept of self-directed IRA has

been introduced for quite a long time now, but people are still not comfortable

with the idea and have various concerns about it.

There are multiple misconceptions about the

use of funds in self-directed IRA that should be clarified for the better

understanding and benefit of common folks

Self-directed IRA is a magnificent

financial tool that can help you to generate a huge amount of wealth easily and

legally. It opens a huge range of investment options for you that can have huge

valuations for your portfolio.

Traditional VS Self Directed IRAs

There is a very small but major

difference between the two types of IRA. The difference is about the authority

of the custodian about the investment restrictions in either type of IRA.

The custodian has a much more active

role in traditional IRA, and it decides the investment direction of your funds.

It usually allows people to invest only in areas like bonds, stocks, annuities,

and mutual funds, and no other form of investment is welcomed.

Whereas, in self-directed IRA, the

custodian doesn’t have that much active role in investment options. The

custodian’s responsibilities are limited to mainly tax management and allow you

to manage your investments as you desire.

Hence, for self-directed IRA, one can have multiple investment options, in addition to the traditional options, like real estate investment, new start-ups, cryptocurrency, etc.

Self-Directed IRA Misconceptions

Many people have certain misconceptions about the mechanism and processing of the self-directed IRA.

These misconceptions misguide them badly and lead to bad investment decisions and negative financial consequences. So, here we have enlisted all these major concerns to clarify them once and for all.

1. The first misconception is about investment options. As discussed above, traditional IRAs have a limited room for investment options. The reason for the fixed policy is that conventional markets are relatively easier to engage with and monitor compared to alternative options.

For example,cryptocurrency is a very risky investment option that can be unacceptable for traditional IRAs. On the other hand, the self-directed IRA has no such issues and are open to every kind of investment option.

2. The next misconception about self-directed IRAs is that these firms have absolute authority over the money. Whether traditional or self-directed, no IRA firm has any such authority. Their mere responsibility and control are about keeping your money safe.

They can’t invest your money without your permission, and even after investing, you have the authority to cancel their access to your funds.

3. Another common misunderstanding of people is that real estate investments in self-directed IRAs could be used personally. It is not true at all. The only purpose of the IRA-based real estate investment is to make a profit. You can’t use the property or live in it.

4. The biggest misconception of self-directed IRAs is about their legality. The non-traditional investments are generally considered illegal.

Cryptocurrencies, tax liens, venture capitalism, etc. all these are legal forms of investment, where markets are regulated by safety measures and laws.

Uncertainty is at the core of investment. Just because alternative investment options are not widely discussed doesn’t elevate them as riskier than traditional methods.

Real estate is the safest investment option while cryptocurrency is volatile but not overly risky.

Even in traditional investment options like bonds

and stock, uncertainty is inevitable. The more you concentrate on one specific

market the higher the risk will be. In any investment market, the simple and best

way to avoid risk is diversification.

Conclusion

The self-directed IRA makes you more empowered concerning your fund investment.

You have more liberty to make more money compared to traditional methods by adopting alternative ways.

Take advantage of the greater options and the possible gains available for you and get benefited excessively in your future.

ETFs belong to a growing sphere of investment that hugs the headlines in financial markets around the globe. Here are important strategies for trading in them.

ETF Strategies for Traders

ETFs usually track

the bonds, stocks or index, and other securities. These can be extensive market

indexes like Nasdaq or Bloomberg Barclays US Aggregate Bond Index, targeted

regional indexes, or niche indexes.

ETF might have hundreds of securities in their portfolio that tend to create prompt diversification to help in reducing the risk, as compared to owning individual stocks.

There is also some chance to further expand by structuring a basic portfolio with multiple ETFs. Each of these ETFs will hold a different type of security across asset classes.

ETF adoption is

growing fast due to being a tax-efficient mode to continue with your investment

ideas and through providing a low-cost and flexible mean to enter the potential

of the markets.

At the start of the 21st century, the ETF assets were even less than $100 billion. Now, by 2018 the ETF assets have exceeded $4.7 trillion around the world and are still increasing its number of products.

According to an estimation by BlackRock, by 2023, ETF assets will rise to more than $12 trillion.

Let’s have a

look at each of its characteristics in detail.

Choice

First of all, you

need to determine what you are looking for. Whether you are a retiree that is

shopping for funds to have some speedy source of income, or you are a

Millennial who has just switched his job and now trying to find a way to roll

over your assets so that they could help them after retirement.

There are almost

1800 ETFs that are enlisted in the US, and BlackRock’s ETF business, iShares

have about 300 to offer just in the US, and more than 800 around the world,

which represents a huge range of geographical regions and asset classes.

You have the option

to select an ETF portfolio that is most suitable for you, your passion and your

goals.

Do you want to

reflect your value through your money? With viable iShare ETFs, you don’t need

to go against your personal beliefs while investing.

For example, if you are an environmentalist,

you can always invest in companies dedicated to providing positive

environmental, governance and social business practices.

Or if you want to

invest in some long-term future-shaping forces, like rising technology, various

ETFs are there offering collaboration with companies that work in technological

advances and also working to shape our global society and economy.

Value

Investing in mutual

funds that are being actively managed can be a bit costly as their professional

asset managers and all the researching staff has to be paid for their working

and the decisions they make.

iShares ETFs

usually charge a very small amount of fees. It can be said that iShares ETFs

charged fees in on average, one-third of an active mutual fund, and still they

generate half the tax compared to the average of an active mutual fund.

The value keeps

adding up. By 30 years, hypothetical investment of $10,000 made in an active

open-end mutual fund with a fees of 0.96%, the monthly assistance of $1,000 and

an expected compounded rate of 8% for return, will be likely to grow to an

amount of $1.2 million and is going to lead to $270,000 in the fees.

Keeping every other

calculation same for an ETF charging 0.34% fees, it will be likely to rise up

to $1.4 million and leading to just $100,000 in fees.

Accessibility

Get in the game without any hassle. One of the major benefits of ETFs is that you can sell and buy them all day round, similar to stocks. What you need for that is just a brokerage account.

For a mutual fund, you need to buy and sell typically through a mutual fund broker. You will get your reimbursement three days after you place your order, but according to the net value of the asset of the day when you placed your order.

But with ETFs, you don’t need to wait that long. Markets are open all the time and you can sell out whenever you want and get you to cash at the moment.

For some mutual

funds, there is a limitation of buy-in or minimum amount that you have to

invest. But there is no such limitation with ETFs. Buy your shares just as you

buy stocks for individual companies without any minimum share. If you can

afford the share price, you can buy it without any condition.

These differences

make ETFs for young investors worth considering. You can also use ETF as a

modern-day gift to cherish major events in your life like wedding, graduation,

communions, etc.

iShares ETFs gives

you the opportunity to choose from various options and make the most suitable

choice to assist in your needs, with the transparency and assurance that you

are getting right value for your money and investing in the easiest way that

suits you.

But look at the

bigger picture, you can use the iShares ETFs not only to help you to reach the

goals of your life but also assist you to keep up with your personal passions.

Risks Involved

in Investing, Including the Risk of Loss

The environmental,

social, and governance investment strategy restricts the form and frequency of

the investment choices available to the fund. It usually results in

underperformance of the fund as compared to other funds that do not focus on

ESG.

The ESG strategy of

fund results in major investments in the industry of security fields that lead

to overall market underperformance or underperformance of other funds that are

selected for ESG standards.

Those funds that

tend to concentrate their investments in specific sectors, industries, asset

class or market might underperform or can be more volatile compared to other

sectors, industries, asset classes or markets than the general securities

market.

Conclusion

Technology companies tend to be more affected by product obsolescence and excessive competition. ETFs as well as shares’ transaction lead to commissions of brokerage and ultimately generate tax. Every investment company has to distribute portfolio returns to shareholders.

The fees related to funding investment are not just borne by the investors in individual bonds and stock. The investment comparisons are only for explanation. To have a better understanding of the differences and similarities between investments one must read the product prospectuses.